min read

Recently, I noticed a new credit card offer that sounded great. So, naturally, I clicked on the ad. Instead of sending me to a separate landing page with more information, I was unpleasantly surprised when the ad re-directed me to the bank homepage. Annoyed, I continued my online banking. However, while they lost me with that online banner, the campaign was multichannel and still managed to pull me in.

I received another ad after logging into the bank system. It came in the form of a message suggesting that I call the contact center to order this new card. I was not keen on talking to the interactive voice response (IVR) system I was initially confronted with so I messaged the bank. After some back and forth email communication, eventually I was put in contact with someone at the call center.

Once the card was ready, I received a text message saying I had to pick it up in person. This was a nice touch, except I was given no branch address or any details regarding a time for collection. I had to contact the call center again. This time around they provided me with incorrect information, causing me to visit the branch twice in order to get my card.

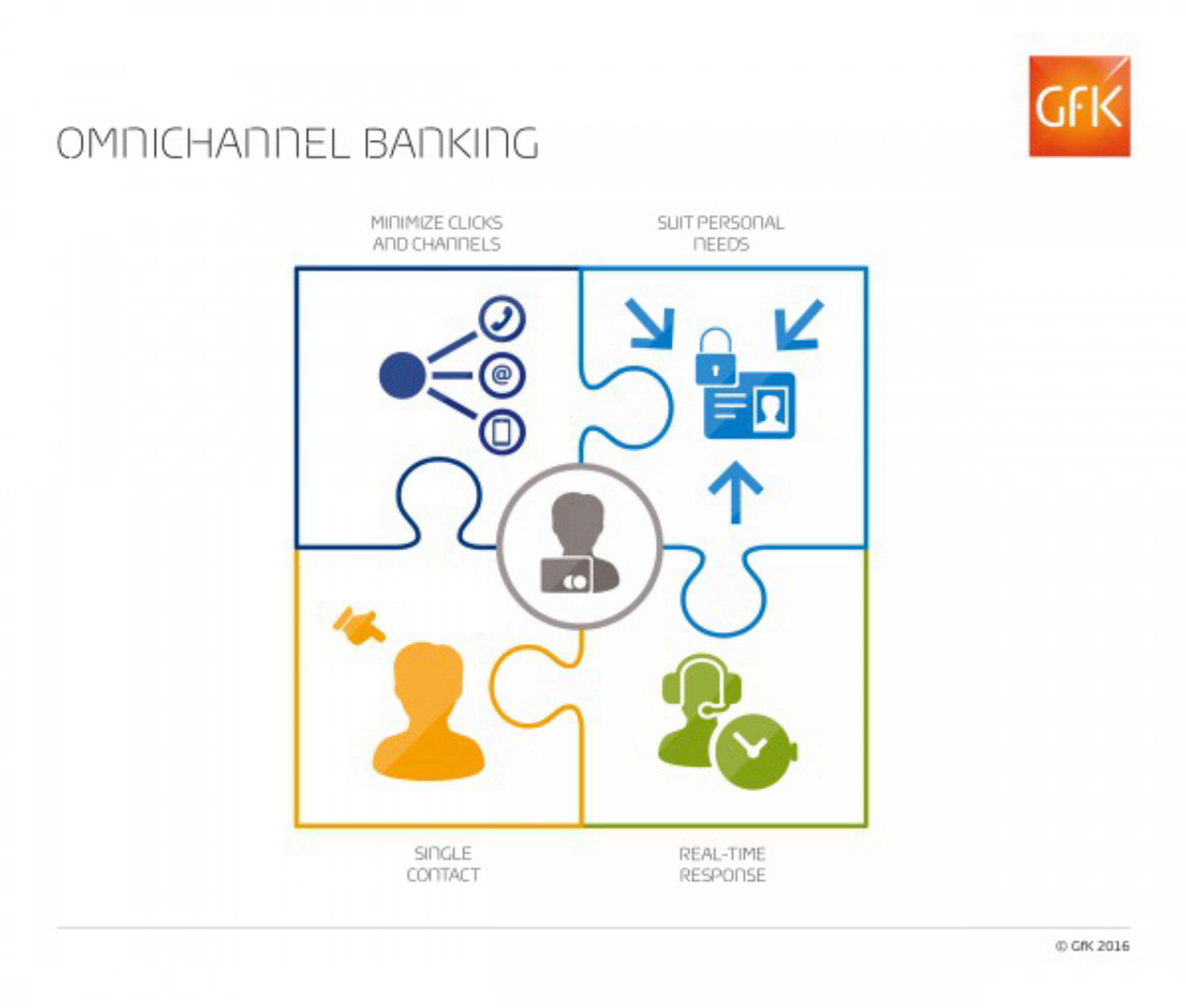

Minimize, differentiate, accelerate, and connect omnichannel banking

I was dissatisfied. But as a marketer, I started thinking about how this irritating experience could be fixed – what would the seamless customer journey look like?

- Minimize clicks and channels

In this case I had to interact with the bank using six channels with two or more interactions within each channel. Simply put, limit the clicks and channels.

- Differentiate channel experiences to individual needs

As I consider myself to be both technically advanced and busy, I would expect the bank to cater to my needs and provide a fast, single-channel and remote solution for obtaining the card. At the same time, there are individuals to whom the card is targeted at who prefer not to receive cards in the mail because of privacy concerns. It’s essential to differentiate to fit individual needs.

- Real-time interaction across channels

If the bank decides to add multiple remote channels it should ensure the response time is the same as it would be if the customer were to enter the branch or call the center, i.e. “real time”. Most of us would certainly not expect to wait in line for a couple of days, so we should we wait this long for an email?

- Multiple channels – single contact

It is paramount for banks to have a single contact person across channels, or at least have representatives with instant access to the same level of information about customers.

Will banks eventually listen to feedback?

I sent those recommendations to my bank, and I hope that they are useful in helping them ensure a seamless omnichannel journey for other online bankers.

Please email me your thoughts at Dmytro.Yablonovskyy@gfk.com.